Name of QuantLet: IDA_FRMspillover

Published in: Institute for Digital Assets (IDA)

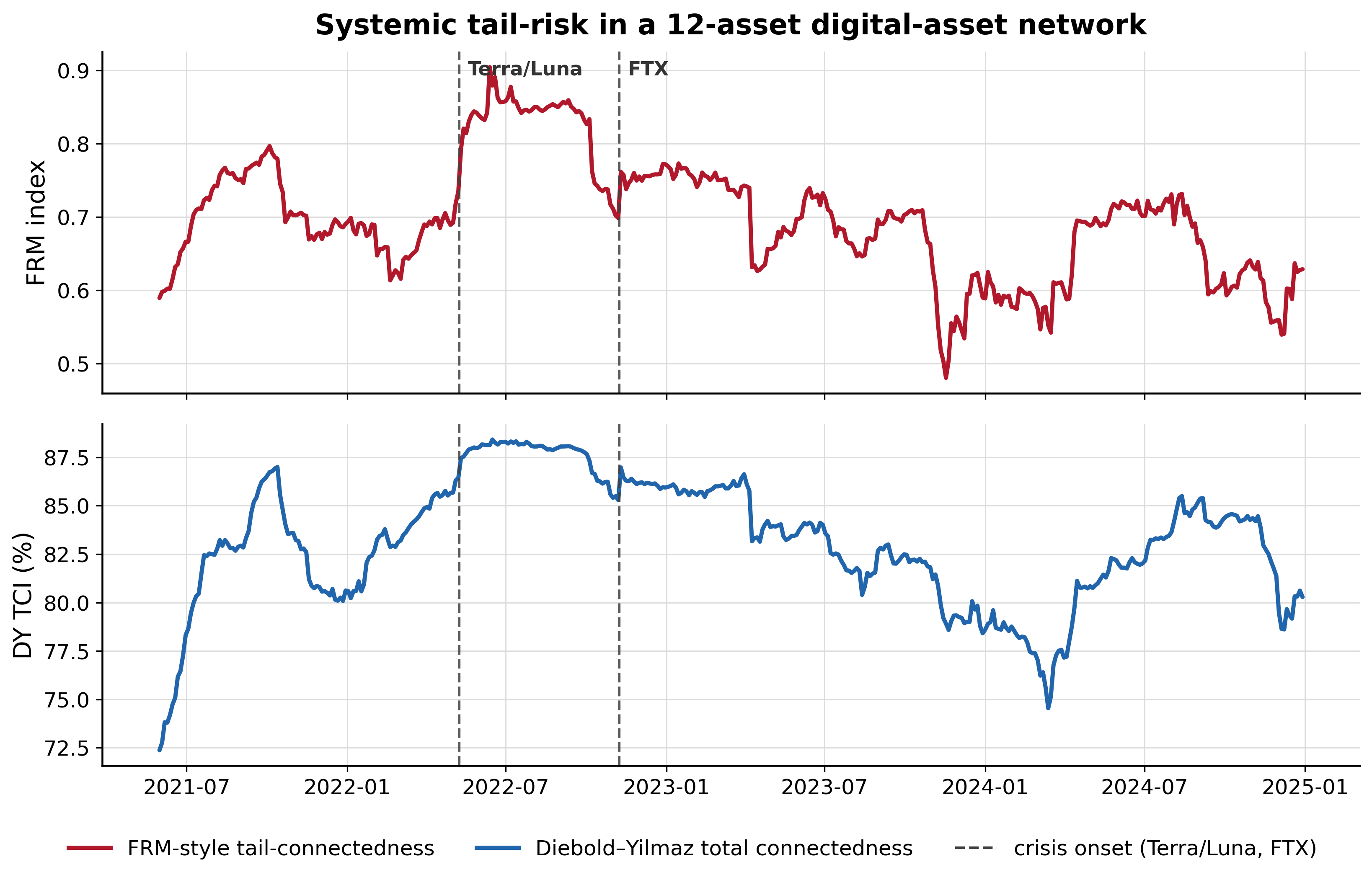

Description: Computes two systemic-risk indices on the same rolling windows of real daily digital-asset returns (12 liquid assets, 2021-2024, Yahoo Finance): an FRM-style tail-connectedness index (mean L1 norm of penalised 5% quantile-regression coefficients of each asset on the others, a Haerdle-FRM proxy) and a Diebold-Yilmaz total connectedness index from a VAR(1) generalised forecast-error-variance decomposition. The FRM-style index is elevated and rising into the Terra/Luna collapse (May 2022) but does not locally lead the idiosyncratic FTX failure (Nov 2022) - the contrast motivating a finite-sample reliability theory for systemic tail-risk meters.

Keywords: FRM, financial risk meter, systemic risk, tail risk, quantile regression, LASSO, connectedness, Diebold-Yilmaz, spillover, cryptocurrency, network, VaR

Author: Daniel Traian Pele

Submitted: 25 June 2026

Datafiles: prices_cache.csv

Output: systemic_indices.png, systemic_indices.csv, poc_results.md

Example: systemic_indices.png - FRM-style tail-connectedness index (top) and Diebold-Yilmaz total connectedness index (bottom) on a 12-asset digital-asset network, with the Terra/Luna (May 2022) and FTX (Nov 2022) onsets marked.

{kind=link}